rewrite this content using a minimum of 1000 words and keep HTML tags

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $171.21 (-1.0%)

EPS YoY +19.2%|Rev YoY +7.4%|Net Margin 16.3%

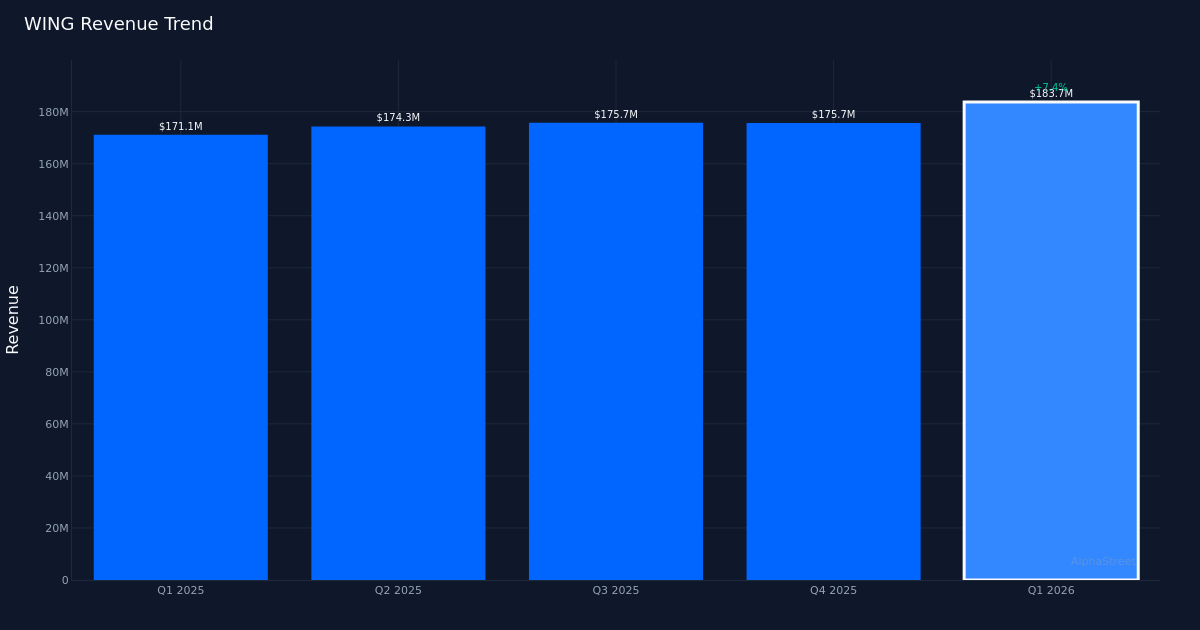

Wingstop (WING) delivered a convincing earnings beat in Q1 2026, but the 12.4% upside surprise masks a fundamental tension between aggressive unit expansion and negative same-store sales momentum. The company reported adjusted EPS of $1.18 against estimates of $1.05, representing 19.2% year-over-year growth from $0.99 in Q1 2025. Revenue climbed 7.4% to $183.7M from $171.1M, though this topline expansion was driven entirely by opening 97 net new restaurants rather than productivity gains at existing locations.

Earnings quality reveals a company leveraging its asset-light franchise model to sustain profitability despite operational headwinds. Net income plunged to $29.9M from $92.3M year-over-year. Net margin contracted to 16.3% from 17.1%, a decline of 0.8 percentage points. Operating margin of 27.4% and EBITDA of $57.2M demonstrate the franchise model’s inherent leverage, but the year-over-year margin deterioration suggests this wasn’t a clean beat. Management emphasized the EBITDA performance, noting “In the quarter we delivered double digit adjusted EBITDA growth, and we opened 97 net new restaurants translating into 17% unit growth,” but the compression at the net income level indicates rising costs below the operating line are eroding profitability faster than revenue is scaling.

The revenue trajectory shows sequential acceleration across four consecutive quarters of growth, though the quality of that growth warrants scrutiny. Revenue progressed from $174.3M in Q2 2025 to $175.7M in Q3 2025, held at $175.7M in Q4 2025, and jumped to $183.7M in Q1 2026. This represents the strongest quarterly revenue in the trailing four periods, but the 4.6% sequential gain from Q4 to Q1 stands entirely on new unit economics rather than comparable store productivity. The domestic same-store sales decline of 8.7% is particularly concerning given the restaurant industry’s reliance on comp growth as a proxy for brand health and pricing power. Management acknowledged this dynamic, stating “System-wide sales increased 5.9% to $1.4 billion in the quarter, fueled by net new unit development, and more than offset the 8.7% decline in same-store sales.”

Unit economics appear sufficiently compelling to sustain aggressive expansion despite negative comps. With 3,153 system-wide restaurants now open, Wingstop is expanding its footprint at a remarkable pace. Management highlighted the investment thesis: “We opened 97 net new restaurants in the first quarter, a 17% growth rate, and with domestic AUVs at approximately $2 million on a roughly $580,000 upfront investment to build a Wingstop, our brand partners are seeing on average a payback of less than two years.” This sub-two-year payback period explains why franchisees continue opening locations despite the 8.7% same-store sales headwind. The company operates an asset-light model where franchisees bear capital risk, allowing Wingstop to collect royalties on expanding system-wide sales while maintaining minimal balance sheet exposure.

Management’s guidance reaffirmation signals confidence that unit growth can carry financial performance even as comparable metrics deteriorate. The company reiterated its 15 to 16% unit growth outlook for the full year, implying continued aggressive expansion. Management framed this as “another industry-leading year of unit growth,” suggesting competitive positioning remains intact despite operational challenges. The willingness to maintain guidance after a quarter of negative 8.7% comps indicates either expected sequential improvement in same-store sales or confidence that the franchise model’s economics can absorb continued weakness at the store level. Management’s commentary acknowledged the tension directly: “Obviously, the comp growth isn’t where they want it to be, but past couple of years sales growth, the 70% type returns they’re generating, all that supports the outside unit growth.”

The market’s muted 1.0% decline in the stock price to $171.21 suggests investors are weighing the earnings beat against the same-store sales deterioration. This restrained reaction indicates the market had likely anticipated weak comps but is giving management credit for maintaining unit economics and margin structure. The stock’s resilience despite negative same-store sales growth reflects investor confidence in the franchise expansion strategy, though sustained comp weakness could eventually pressure franchisee willingness to deploy capital into new locations.

The fundamental question facing Wingstop is whether negative same-store sales represent transitory consumer softness or structural market share loss. A company can grow through unit expansion for extended periods, but the franchise model’s sustainability depends on existing operators remaining profitable enough to reinvest. At 100% beat rate over the last quarter, Wingstop is executing against lowered expectations, but the 8.7% same-store sales decline presents a clock on how long expansion can compensate for productivity loss.

What to Watch: Q2 same-store sales trends will determine whether the 8.7% decline represents a cyclical trough or the beginning of sustained productivity erosion. Monitor franchisee development commitments and whether the 97-unit quarterly pace proves sustainable throughout 2026. Net margin trajectory matters more than topline given the asset-light model—further compression below 16.3% would signal the unit economics story is deteriorating faster than expansion can offset.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

and include conclusion section that’s entertaining to read. do not include the title. Add a hyperlink to this website http://defi-daily.com and label it “DeFi Daily News” for more trending news articles like this

Source link