rewrite this content using a minimum of 1000 words and keep HTML tags

Quick Breakdown

The digital euro aims to make domestic and cross-border transactions faster, cheaper, and more secure while improving financial inclusion and access to central bank money for all citizens and businesses.

Beyond convenience, the initiative is a strategic move by the European Central Bank to reduce reliance on non-European payment systems, enhance monetary policy control, and protect the euro from geopolitical and financial pressures.

The digital euro seeks to offer a state-backed alternative to private stablecoins and Big Tech solutions, carefully balancing user privacy, regulatory compliance, and opportunities for fintech innovation.

The digital euro is a proposed Central Bank Digital Currency (CBDC), currently being developed by the European Central Bank. Its purpose is to work alongside cash and existing electronic payment methods across the euro area, not replace them entirely. In simple terms, the project is meant to modernize the way money moves in an increasingly digital economy, while giving people a public, state-backed option instead of relying only on private payment platforms. Supporters argue that it could make everyday transactions quicker, less expensive, and more secure for both consumers and businesses throughout Europe.

Still, the push for the digital euro is about far more than convenience at the checkout counter. As CBDCs continue gaining traction around the world, Europe has become increasingly dependent on non-European payment companies and outside financial infrastructure. That reality has sparked a much broader conversation, and honestly, it is one that reaches beyond technology itself. Is the digital euro really just a tool for smoother and more efficient payments, or is it part of a larger strategy to defend Europe’s financial sovereignty in a fast-evolving global economy?

Payment Efficiency Benefits for Citizens and Businesses

A core argument for the European Central Bank’s digital euro is that it modernizes Europe’s payment system. So how will the digital euro work? It’ll make everyday transactions more efficient, resilient, and accessible for both citizens and businesses.

Faster, cheaper domestic and cross-border payments

The digital euro could drastically reduce the time it takes to send money across countries in the eurozone, eliminating delays caused by correspondent banking networks. Transaction fees would also drop because there would be fewer intermediaries and reduced dependence on legacy infrastructure, benefiting both small-scale retail transfers and high-volume business transactions.

Reduced reliance on intermediaries and card networks

By allowing direct peer-to-peer payments between citizens or businesses, the digital euro could bypass banks and card networks for routine transactions. This reduces costs, lowers counterparty risk, and strengthens European sovereignty over its own payment ecosystem, which is increasingly dominated by global tech and finance companies.

Financial inclusion and public access to central bank money in digital form

Unlike traditional bank accounts, which may exclude some groups due to credit checks or minimum balances, a digital euro wallet could give all citizens direct access to central bank funds. This ensures secure, public-backed money is available to everyone, including rural populations, students, and those underserved by private banking systems.

Improved resilience of the payments system

A central bank–backed digital currency would provide a stable fallback during technical failures of private networks or in times of financial stress. By maintaining a guaranteed, functional payment option, the digital euro could prevent disruptions that might otherwise paralyze commerce or public services in emergencies.

Greater transparency and security in transactions

European Central Bank’s digital euro payments could include cryptographic safeguards and standardized reporting, making it harder for fraudsters to manipulate transactions.

Businesses could benefit from real-time tracking, easier reconciliation, and reduced errors, while regulators gain better oversight to detect suspicious activity without compromising user privacy.

Better foundation for future financial innovation

With programmable features and public oversight, the digital euro could support emerging financial technologies, such as automated payments for subscriptions, smart contracts for trade settlements, or tokenized assets. This creates a reliable infrastructure for innovation without exposing the system to the risks of unregulated private platforms.

Strategic Financial Independence

The digital euro isn’t just about speed or convenience; it also represents Europe’s bid to assert greater control over its financial system and reduce dependence on external powers.

Europe’s reliance on non-European payment systems and infrastructure

Currently, many cross-border payments rely on networks and platforms based outside the eurozone, exposing Europe to foreign fees, delays, and potential restrictions. By introducing a digital euro, the EU could reduce dependence on these non-European systems, ensuring that citizens and businesses can transact securely within a homegrown framework.

Digital euro as a hedge against geopolitical and financial fragmentation

Global tensions and sanctions can disrupt access to foreign payment networks, leaving European businesses vulnerable. A European Central Bank’s digital euro would provide a stable alternative, insulating the economy from political pressure and creating a financial tool that remains fully operational regardless of external disruptions.

Strengthening control over monetary policy transmission

By providing a digital form of central bank money directly to citizens and businesses, the European Central Bank can more effectively implement monetary policy. Interest rate adjustments, liquidity injections, or emergency measures can be transmitted faster and more uniformly, ensuring policy goals are met and the euro retains its stability across the region.

Enhancing domestic and regional sovereignty in finance

A widely adopted EU Central Bank digital currency would allow Europe to keep critical financial data, transaction flows, and currency reserves within its own jurisdiction. This reinforces autonomy over payment monitoring, regulatory compliance, and systemic risk management, reducing reliance on foreign oversight or proprietary systems.

Reducing exposure to foreign currency dominance

Currently, large global payments often default to dollars or other major currencies, limiting Europe’s ability to control its own financial ecosystem. A digital euro could encourage the euro’s use in international trade and settlement, boosting the currency’s influence while reducing dependency on external monetary policy.

Building a foundation for resilient, pan-European financial infrastructure

By integrating the digital euro into existing European payment rails and emerging technologies, the EU can develop a robust, interoperable system. This strengthens cross-border commerce, supports digital innovation, and ensures the eurozone can act cohesively in times of economic or geopolitical stress.

RELATED:

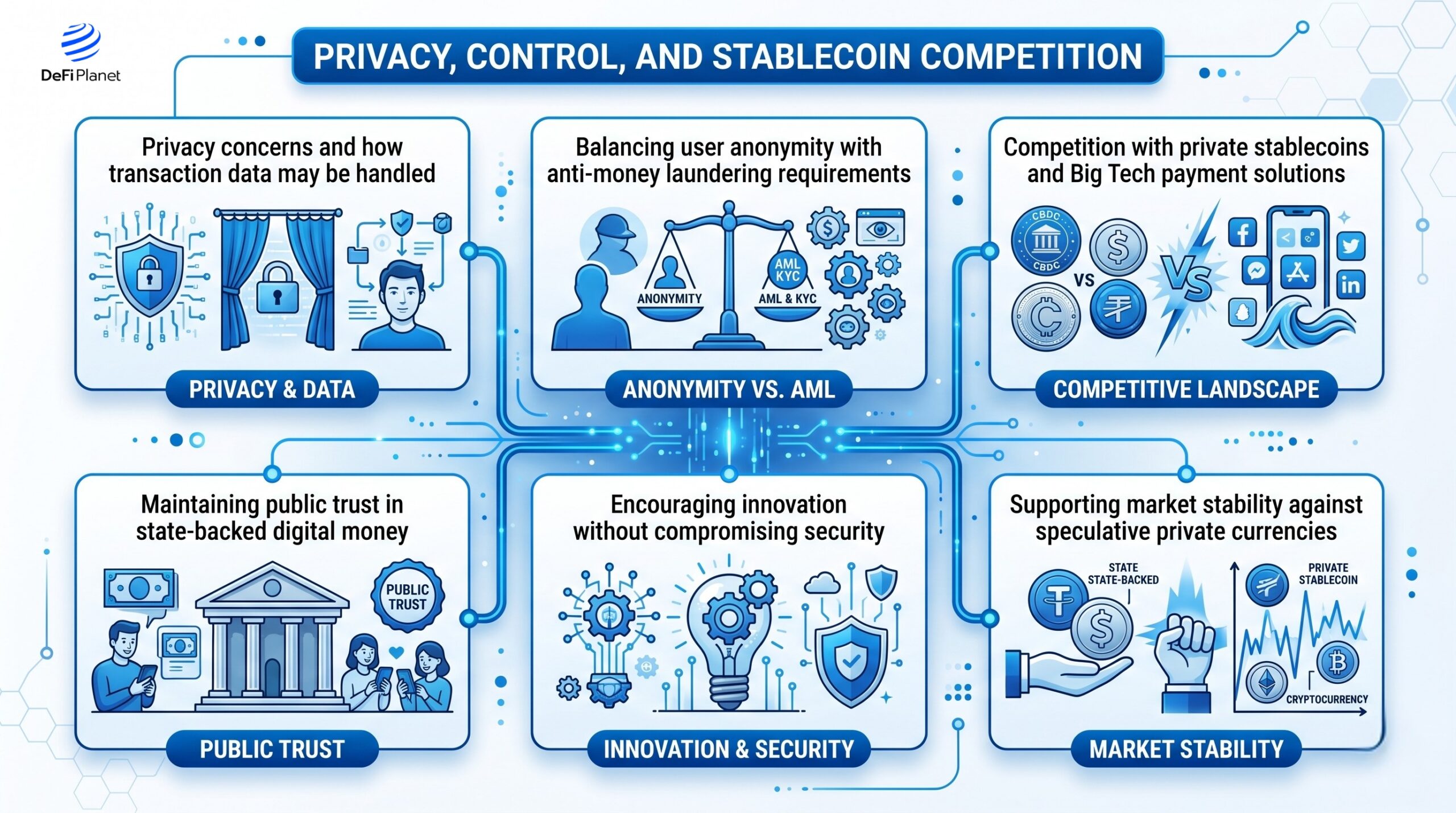

Privacy, Control, and Stablecoin Competition

The digital euro raises important questions about who controls financial data and how Europe competes with private alternatives in a rapidly evolving payments space.

Privacy concerns and how transaction data may be handled

A central feature of any CBDC is the ability to track transactions, which can clash with citizens’ expectations of financial privacy. The European Central Bank’s digital euro must find ways to protect user information, ensuring that spending habits or account balances aren’t unnecessarily exposed while maintaining trust in a government-backed system.

Balancing user anonymity with anti-money laundering requirements

European regulators must walk a fine line between safeguarding user privacy and preventing illicit activity. Unlike cash, digital euro leaves a traceable record, which is essential for combating money laundering, terrorist financing, and fraud, but excessive surveillance could undermine public confidence and adoption.

Competition with private stablecoins and Big Tech payment solutions

Private stablecoins and platforms from companies like Apple, Google, or Meta offer fast, convenient payment options, often with integrated wallets and loyalty features. The EU Central Bank digital currency aims to provide a public alternative that ensures sovereignty, keeps transaction fees within Europe, and prevents dependence on foreign or corporate-controlled systems.

Maintaining public trust in state-backed digital money

As citizens weigh privacy against oversight, the ECB must design the digital euro to be transparent and reliable. Clear rules on data retention, anonymization, and access will be critical to ensuring users trust the digital euro over private solutions or offshore stablecoins.

Encouraging innovation without compromising security

To compete with tech-driven alternatives, the digital euro could enable programmable features, micropayments, and integration with fintech apps, all while adhering to strict privacy and compliance standards. This balance could spur innovation within Europe while keeping users’ financial data under public control.

Supporting market stability against speculative private currencies

Stablecoins can experience volatility or fail if not properly collateralized, risking user funds and systemic stability. A well-designed digital euro offers a secure, fully backed alternative, reducing reliance on potentially risky private coins and reinforcing the euro’s role as a stable, trustworthy unit of exchange.

Which Goal Drives the Digital Euro?

The EU Central Bank digital currency is often presented to the public as a tool for faster, cheaper, and more convenient payments, highlighting benefits for everyday users and businesses. Domestic transfers could settle instantly, cross-border payments would be smoother, and reliance on costly intermediaries like card networks or foreign processors could decrease. These features make the digital euro attractive for citizens, offering a modern alternative to cash and traditional banking methods.

However, beneath the convenience lies a more strategic mission: financial independence and monetary sovereignty for Europe. By issuing its own CBDC, the European Central Bank strengthens control over monetary policy, reduces reliance on foreign payment rails, and ensures that the euro remains competitive in a global financial system increasingly influenced by private stablecoins and Big Tech payment platforms.

Although convenience is the public-facing benefit, the primary driver is sovereignty first, user convenience second. Europe wants a state-backed digital currency that safeguards its economic autonomy, protects citizens from external shocks, and preserves the euro’s global influence.

Conclusion: The Future of the Digital Euro

The European Union’s Central Bank Digital Currency is shaping up to become a defining piece of the next chapter in European finance if it sails successfully. It has the potential to change how citizens, businesses, and governments handle everyday transactions, not just by making payments more convenient, but by building a stronger and more independent financial system. In many ways, the digital euro represents Europe’s attempt to reduce its reliance on global card networks, major tech companies, and foreign currencies that currently dominate large parts of the payment landscape. That shift could give the region far greater control over its own financial future.

Looking ahead, the digital euro may also reshape cross-border trade, improve financial inclusion, and open the door to new digital services operating on a secure platform backed directly by the central bank. And honestly, that is where things start to get really interesting. If implemented carefully, it could become more than just another payment tool sitting on your phone beside five other apps nobody remembers downloading. It could evolve into a core pillar of Europe’s digital economy.

Still, the project’s long-term success will depend on striking the right balance between innovation, privacy protections, regulation, and technological reliability. Europe is trying to walk a pretty fine line here: embracing digital efficiency without sacrificing public trust or monetary sovereignty. If policymakers manage that balance well, the digital euro could place Europe at the forefront of the global shift toward digital finance. And if not, well, even the smartest financial experiment can end up collecting dust like an old app update everyone ignored.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics tools.”

and include conclusion section that’s entertaining to read. do not include the title. Add a hyperlink to this website [http://defi-daily.com] and label it “DeFi Daily News” for more trending news articles like this

Source link