rewrite this content using a minimum of 1200 words and keep HTML tags

Analyst Weekly, December 8, 2025

A BOJ hiking cycle could be 2026’s biggest macro plot twist.

After years of snoozing near zero, Japan’s 10-year government bond yield (JGB) is ripping higher into year-end, inching toward 2% & higher. For a country that’s lived with ultra-low rates for a generation, this is a seismic shift.

What’s driving the surge? Sticky inflation + a fiscal hangover

Japan finally has inflation, the kind it actually wanted for years, but now it won’t go away. The CPI has averaged around 3% since 2022, well above the Bank of Japan’s target, while policy rates have barely budged.

Add in Japan’s eye-watering 237% debt-to-GDP ratio and a BOJ balance sheet stuffed with long-dated bonds (with higher interest rate sensitivity), and the market is losing patience. The BOJ today is facing the same problem the Federal Reserve ran into during the 2022-2023 hiking cycle: large, unavoidable mark-to-market losses on the massive bond portfolio it accumulated during years of QE.

Investors want compensation for rising risks, and yields are moving up to deliver it.

Why global investors care: Japan’s moves don’t stay in Japan

Japan is one of the world’s biggest buyers of US Treasuries and global sovereign bonds. When JGB yields spike:

Carry trades unwind, adding volatility to equities.

Global long-end yields rise as Japanese investors bring money home.

The US Treasury curve steepens, pressuring mortgage spreads (MBS) and long-duration assets.

In short, if JGB yields keep climbing, the “safe” part of global portfolios could get shaken up.

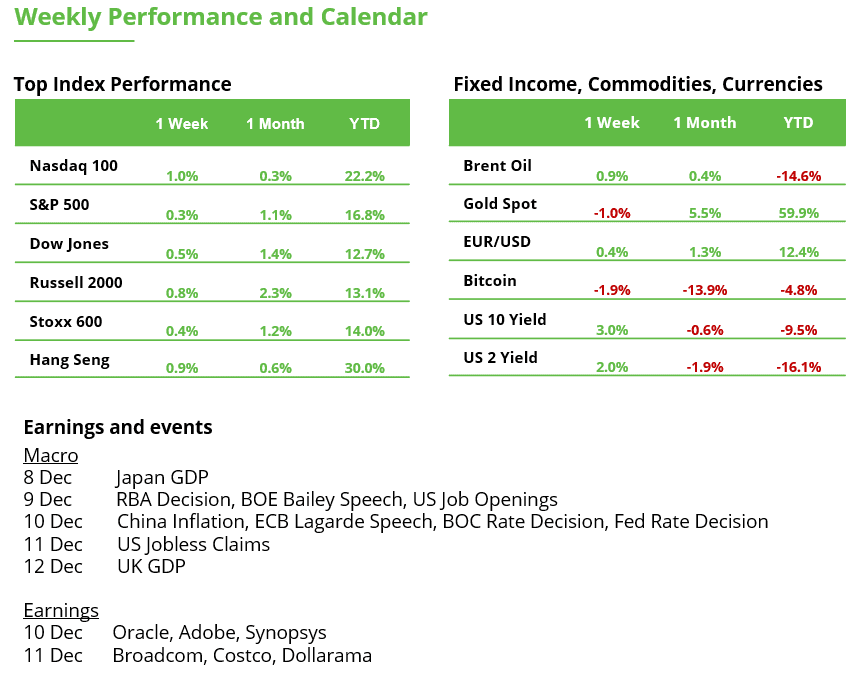

US: When the Real Economy Stocks Start Talking, Investors Listen

Market mood is shifting: instead of a handful of mega-caps steering the ship, a wider mix of economically sensitive sectors is starting to participate.

It’s the kind of broadening that tends to get investors’ attention, and we think that markets are pricing in an accelerating macro activity in 2026, especially as strength shows up across banks, transports, energy (early stages), and even global FX.

REITs remain the clear laggard, though healthcare-focused names are quietly gaining share. Overall, markets are sending a broader, and a more economically grounded message, even as lagging indicators (such as unemployment data) continue to remain weak in Q4 (and possibly into Q1 2026).

The Big Picture

1) Cyclicals are showing signs of life

Equal-weight indices, small caps, banks, and industrials have all pushed higher, a tone that typically shows up when market confidence in the economic backdrop firms.

Investor Takeaway: Some investors view broader participation as a healthier market pattern, particularly when small caps and cyclical groups join the move.

2) Housing and Energy add some spark

Homebuilders saw one of their strongest 10-day surges in years, while equal-weight Energy reached an eight-month high.

Investor Takeaway: Momentum in these pockets often reflects shifting expectations around growth and rates, themes that many market participants keep on their radar when positioning.

3) Global signals lean constructive

Japan’s major indices held up even as local yields climbed, and EM currencies touched a 52-week high with help from MXN, BRL, and ZAR. Meanwhile, the US dollar lost some steam near its 200-day average.

Investor Takeaway: Stronger EM FX can indicate improving sentiment outside the US, a trend global allocators tend to watch closely.

Under the Hood

Large banks broke higher after a multi-month pause, and regionals pushed toward recent highs as the yield curve re-steepened.

Investor Takeaway: The group often responds to shifting rate expectations, making it a place where some investors gauge broader risk appetite.

Industrial stocks saw their first meaningful expansion in 20-day highs since early summer.

Investor Takeaway: When transports perk up, some see it as a read-through on underlying economic activity.

Semis rebounded from an oversold backdrop. Breakouts in ADI, AMAT, and strength in ASML suggest momentum is broadening beyond headline names.

Investor Takeaway: Follow-through in semi equipment sometimes aligns with healthier industry cycles.

REITs remain under pressure, despite shifting rate expectations. Healthcare REITs, however, have quietly climbed the sector rankings.

Investor Takeaway: The divergence inside the REIT space highlights how uneven performance has become across rate-sensitive pockets.

Broadcom Earnings: Can the AI Story Withstand Valuation Pressure?

Broadcom will release its quarterly results on Wednesday after the market close. Its core business, semiconductors and hardware, operates in highly competitive markets. At the same time, companies like Alphabet and Broadcom itself are making noticeable progress in the AI chip segment. Competition is intensifying, and the market structure could shift over the long term.

Investors have recently turned more cautious, and the stock fell 3% last week. With a forward P/E of 46.3, Broadcom is highly valued. To justify this level, either the share price must come down or earnings expectations must rise. Operationally, however, the company remains strong, as reflected by its LTM EBIT margin of 39.6%.

From a technical perspective, several support zones lie close together: the fair value gap between $310.47 and $332.83, the recent short-term low at $328.57, and the 20-week moving average at $334.23. The RSI sits at 68, indicating that the market is not overbought. As long as the lower boundary of the gap holds, there is little to suggest that the uptrend will end. A break below that level, however, would require reassessing the situation.

Key questions for the earnings release include whether Broadcom will raise its outlook and whether strategic adjustments are planned—particularly in the AI segment, pricing strategy, or capacity expansion. It will also be crucial to see how the market reacts to margins, order intake, and the updated guidance.

Broadcom, weekly chart. Source: eToro

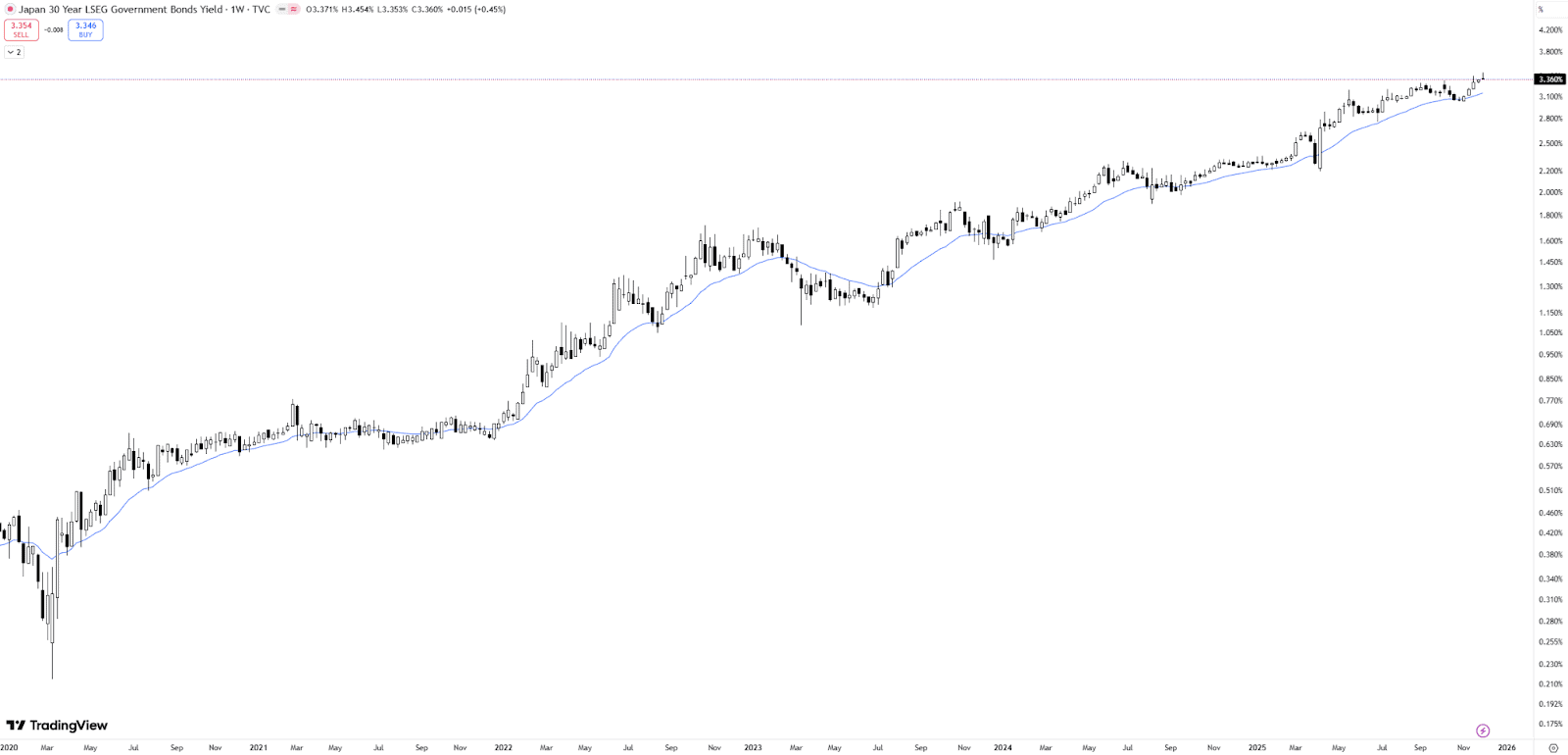

Japan’s Long-Term Yields Climb: Multi-Year Uptrend Intact

The yield on 30-year Japanese government bonds has been in a stable uptrend for years. Last week, it rose again slightly, closing at 3.360% (+0.45%). In an international comparison, Japan now stands roughly on par with Germany (3.442%), while the US remains noticeably higher at about 4.793%.

A continuation of this trend, meaning further rising yields, currently appears most likely. For that to happen, the trend structure must remain intact: higher highs and higher lows are essential.

The picture would become concerning only if the most recent low at 3.026% were to be broken. Just as important is whether the yield falls sustainably below the 20-week moving average, which currently stands at 3.146%. Either development would signal a potential trend reversal or at least a weakening of the upward momentum.

However, chart analysis tells only part of the story. Fundamental factors remain the true drivers. Among them are the Bank of Japan’s policy stance, domestic inflation trends, global capital flows, relative yield differentials, and the movement of the yen.

Yield on 30-year Japanese government bonds. Source: TradingView

Bitcoin’s Big-Decisions Week

Bitcoin’s heading into a stretch where the market may finally pick a lane for the rest of the year. The bounce toward $90K has been solid, helped by a pickup in US demand, but the real battle is at $100K–$103K. That zone has acted as the line between “bull run continues” and “correction incoming” in past cycles.

Flows Say: Stable… but Not Strong

Despite loud headlines, flows paint a calmer picture. New money isn’t rushing in, but institutional holders also aren’t heading for the exits, keeping price structure stable. That said, without fresh inflows, upside moves rely on thinner support. And next week’s monetary policy calls could inject a dose of volatility and shift near-term liquidity.

A Breakout or a Breakdown?

Markets are approaching a fork in the road:

A clean break above $100K: strengthens the case for a resumed uptrend.

A fail or no attempt at all: raises the odds of a longer cooling-off phase.

A drop below $88K: opens the door to deeper doubts.

The next several days of price action will likely set the tone.

The Fragility Factor

The narrative is no longer about price: it’s about liquidity. Trading volumes in both BTC and ETH collapsed over 90% in 48 hours, showing that buyers exist but activity has thinned to the point where even moderate orders can move markets dramatically. This price–activity disconnect is now crypto’s pressure point.

What to Watch

Volume’s Comeback: After the collapse in activity, a rebound in volume is the top signal for whether any move has legs.

Liquidity Quality: Tight spreads + shallow depth = a market that looks stable but can break quickly on big orders.

BTC vs. ETH Relative Strength: ETH’s relative resilience is a read on where institutional interest is sticking, and where it’s fading.

Risk-Asset Correlation: Equities still set the mood. A downturn in stocks could spill into crypto immediately.

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.

and include conclusion section that’s entertaining to read. do not include the title. Add a hyperlink to this website http://defi-daily.com and label it “DeFi Daily News” for more trending news articles like this

Source link