rewrite this content using a minimum of 1200 words and keep HTML tags

DeFi’s latest exploit chatter is pointing traders toward a cost that does not appear in pool APYs: the price of staying connected while bridges, keys, frontends, oracles, and contract logic remain active failure points.

For users and liquidity providers, the question now extends beyond yield. They have to decide how much additional return is needed, even though the route itself can add technical, operational, and governance exposure.

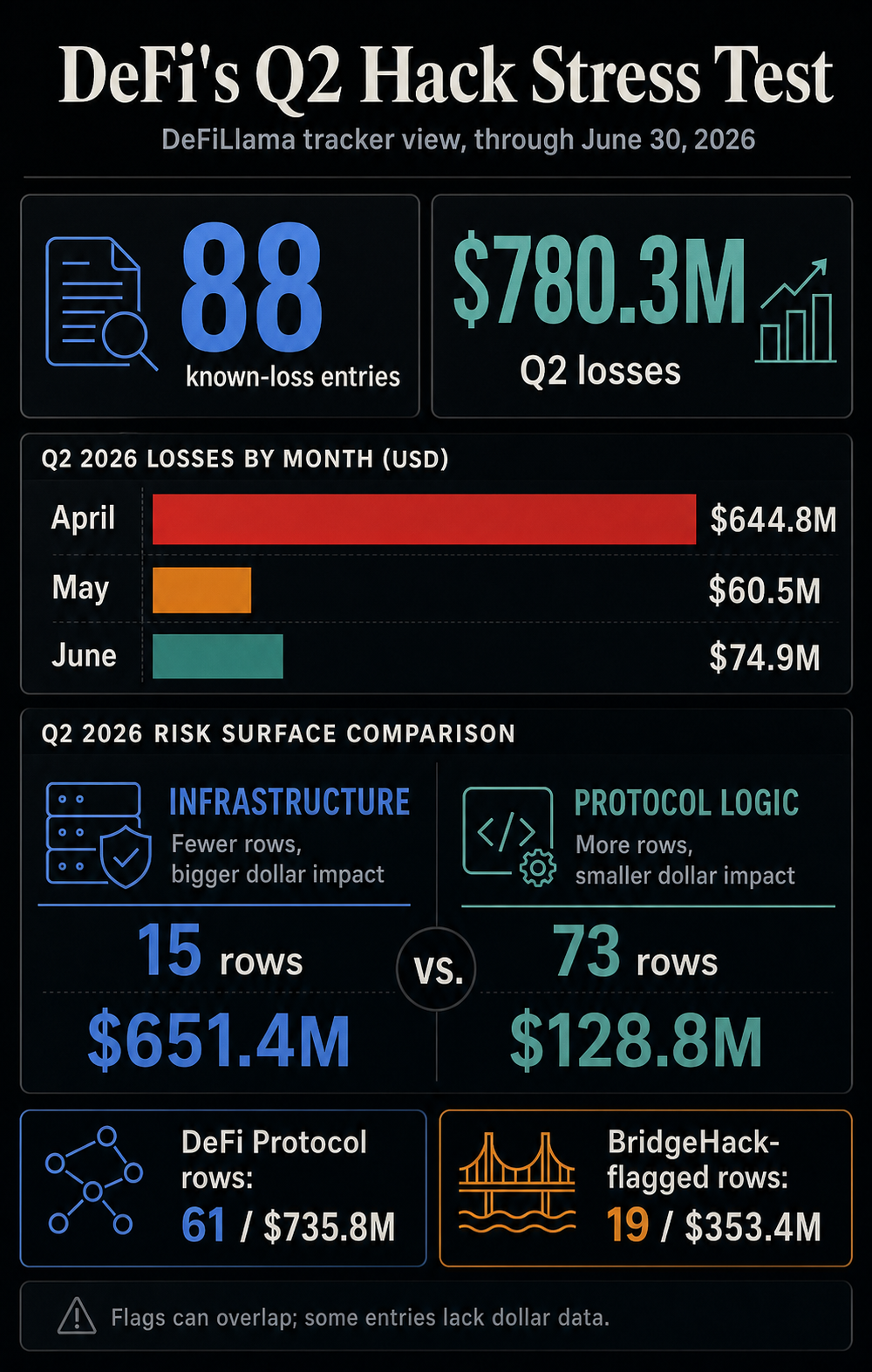

The Q2 dataset behind DeFiLlama’s hacks tracker shows 88 hack entries with known dollar amounts, totaling $780.3 million in losses through June 30.

April carried the largest hit, at $644.8 million, while May and June still added $135.4 million across dozens of entries. The quarter, therefore, looked less like a single blast crater and more like a stress test that kept running even after the headline shock faded.

On June 30, amount-bearing hack entries totaled $16.65 billion. Rows tagged as DeFi Protocol targets accounted for $7.85 billion, while rows flagged as bridge hacks accounted for $3.26 billion.

In Q2 alone, DeFi Protocol target rows accounted for $735.8 million of the $780.3 million total loss, and bridgeHack-flagged rows accounted for $353.4 million.

The dataset needs careful handling. DeFiLlama’s bridge flag can overlap with protocol targets, and some entries have incomplete dollar data.

Even with that caveat, the message is clear: exploit risk is sitting across the routes, permissions, interfaces, and verification systems that make DeFi usable.

The quarter turned security into a price input

Q2 split damage and frequency across distinct risk surfaces. Infrastructure-classified entries accounted for most of the known dollar losses, while protocol-logic entries accounted for most of the incident count.

Q2 2026 DeFiLlama viewAmount-bearing dataTotal Q2 incidents88 entries with known dollar amountsTotal Q2 losses$780.3 millionDeFi Protocol target rows61 rows, $735.8 millionBridgeHack-flagged rows19 rows, $353.4 millionInfrastructure classification15 numeric-loss rows, $651.4 millionProtocol Logic classification73 numeric-loss rows, $128.8 millionMonthly lossesApril $644.8 million, May $60.5 million, June $74.9 million

The distinction changes how risk gets priced. A protocol-logic bug can be treated as a code-quality problem within a single application.

Infrastructure losses are different. They touch bridges, signing systems, cross-chain messaging, admin permissions, hot wallets and other shared surfaces that capital uses to move between venues.

When that layer is under stress, DeFi’s usual yield math starts to look incomplete. A pool can offer a higher return, but users still have to ask whether the route to that return depends on a bridge, oracle, frontend, signer set, or administrative path they cannot evaluate in real time.

A market maker can keep liquidity available across chains only when the spread compensates for the operational risk of moving assets through those rails.

That is the shift from a postmortem market to a live risk-premium market. Participants are repricing the cost of being connected.

The fee is no longer only gas, slippage, or borrowing costs; it also includes the risk that a permission, route, or proof layer fails while capital is in motion.

That repricing can happen quietly. A venue may maintain its advertised annual percentage yield, while the effective return declines as users demand faster exits, insurance, or compensation for bridge exposure.

The market can express that view through thinner liquidity, wider spreads, and more expensive incentives long before a formal security score appears.

Routing trust becomes part of the trade

Bridge exposure is where the stress test becomes easiest to see. Q2’s bridgeHack-flagged rows totaled $353.4 million, enough to make cross-chain routing more than a convenience question.

If capital has to cross a bridge or messaging layer to reach an opportunity, the route itself becomes part of the trade.

Recent cross-chain incidents have already shown how quickly that can affect behavior. The fallout from the KelpDAO and LayerZero exploits showed how a single exploit can push projects to rethink their security infrastructure.

A THORChain halt following an exploit revealed the other side of the same problem: when routing trust breaks down, systems can stop first and ask questions later.

For users, liquidity may move toward venues where the route is easier to understand, where bridge exposure is lower, or where there is enough depth to avoid fragile paths.

For aggregators and market makers, routing logic may increasingly need to include security assumptions alongside price, depth and gas.

That could leave some bridges and cross-chain venues with a higher cost of capital even when they continue to function. Liquidity can still move through them, but it may demand a wider spread, more explicit insurance, stronger proof systems, or shorter exposure windows.

In DeFi, that is what a risk premium looks like before it becomes a line item.

The same logic can affect launch strategy. A protocol preparing a new market may decide that speed is less valuable than a second review of bridge dependencies, admin permissions, or oracle paths.

A liquidity provider may favor fewer chains if each additional route adds a new security assumption. Those decisions are small individually, but together they determine where depth forms and which venues become expensive to use.

Insurance sits inside that same loop. If underwriters and users start treating bridge exposure as a recurring operating risk, coverage becomes another signal about which venues can attract liquidity at scale.

Protocols that cannot explain their assumptions may still operate, but they could pay for that opacity through lower depth or more expensive incentives.

Security spending becomes a distribution cost

The market response also changes inside protocols. Security spending has often been framed as defense: audits, bug bounties, monitoring, incident response, and emergency controls.

A quarter like this makes it part of distribution. If users can tell why one venue is safer than another, security becomes part of how capital chooses where to sit.

Concentration is one reason the issue extends beyond code quality. A TRM Labs analysis described 2026 crypto theft value as concentrated in a small number of large events.

CertiK’s 2026 stablecoin threat work highlights wallet, bridge, custody and payment-infrastructure exposure.

Chainalysis has emphasized threat mechanics such as private-key and signing infrastructure, social engineering, and the speed with which stolen funds can move through laundering channels.

Those firms measure different universes, and Chainalysis’ hard theft totals in the cited post are based on 2025 data. The common thread is still useful: DeFi risk extends beyond bad Solidity.

It includes who can sign, where users connect, how cross-chain verification works, how quickly stolen assets can be swapped, and whether a protocol can detect abnormal behavior before an attacker finishes the route.

That pushes protocols toward spending that looks less optional. Larger bug bounties, real-time monitoring, insurance cover, withdrawal throttles, admin-key controls, proof-system review, frontend hardening and clearer incident communications become part of the trust product.

They also become easier to justify to tokenholders if the alternative is higher liquidity costs after every visible exploit.

The shift in user behavior is the harder consequence. DeFi users have long accepted that smart-contract risk is part of the yield stack, but persistent pressure from exploits changes how that risk is felt.

A single hack can be dismissed as a bad venue. A quarter of recurring incidents makes the whole route feel expensive.

Products that abstract complexity sit directly in that tension. Automated yield strategies, routers, and frontends can make DeFi easier to use, while also hiding the path capital takes.

CryptoSlate has already covered how automated yield products can concentrate retail risk. Under a quarter-long stress test, users may demand more visibility into where funds are routed, what bridge assumptions are involved, what insurance exists, and what happens if a connected service fails.

There is also an outside pressure point. Crypto crime and scam concerns have been pushing the industry toward more self-policing, as shown by Treasury-warning coverage.

The DeFi exploit problem lands in the same market environment: users, venues and policymakers are all asking whether crypto systems can reduce losses without giving up the speed and openness that made them useful.

For DeFi, that is a difficult balance. Add too much friction, and capital routes elsewhere. Add too little, and the risk premium rises after every incident.

The protocols that win the next phase are likely to be those that can demonstrate where the hidden risks lie and what has been done to contain them.

June’s DeFiLlama rows remain an active threat. The month included front-end vulnerabilities, predictable private-key exploits, fake-proof bridges, unbacked mints, reverse MEV, oracle manipulations, and logic or accounting-flaw entries.

No single label explains all of them.

The next signal is whether capital starts moving before the next postmortem. Watch whether bridge liquidity gets more concentrated in venues perceived as safer, whether protocols delay launches for additional review, whether insurance pricing rises, whether bug bounty budgets grow, and whether aggregators make security assumptions more visible in routing decisions.

If those changes accelerate, Q2 will look less like a bad quarter and more like a repricing event.

DeFi’s hack problem would still be a security problem, but it would also become a market-structure problem: a recurring tax on movement, yield, and trust across the systems that make onchain finance work.

and include conclusion section that’s entertaining to read. do not include the title. Add a hyperlink to this website http://defi-daily.com and label it “DeFi Daily News” for more trending news articles like this

Source link

? Binance’s New Reinsurance Token Listing Explained")