rewrite this content using a minimum of 1000 words and keep HTML tags

US President Donald Trump signed an executive order directing a review of regulations and barriers that may limit fintech innovation and restrict access to banking partnerships and payment systems. The move has revived debate around whether fintech companies should be able to access the Federal Reserve’s payment infrastructure more directly.

Should non-bank fintech firms continue to depend on traditional banks to reach payment rails, or should fintechs access central bank payment rails across the US?

TL;DR

US policymakers are reviewing fintech access to Federal Reserve payment systems after an executive order from Donald Trump called for reducing barriers to financial innovation and updating outdated regulations.

At the center of the debate is whether fintech firms should continue relying on banks for access to payment rails or be allowed direct entry into core U.S. payment infrastructure.

The discussion highlights a broader tension between innovation and regulation, as fintech firms push for easier access while regulators focus on stability, oversight, and systemic risk control.

Why Is Access to Fed Payment Rails So Important for Fintechs?

The Fed payment system rails are the core infrastructure that powers how money moves across the US financial system. They handle essential financial activities such as wire transfers, direct deposits, bill payments, and real-time settlements between banks and regulated financial institutions. Because of this role, they sit at the center of how transactions flow through the economy.

Right now, most fintech companies do not have direct access to these systems. Instead, they operate through partnerships with traditional banks that already hold access. This means fintech firms depend on banking partners to process payments, hold customer funds, and settle transactions within the broader financial system.

This structure creates both operational and strategic constraints. Payments often move through additional layers of processing, which can introduce delays, increase compliance requirements, and limit how independently fintech companies can build and scale products. It also means that much of the innovation in digital payments depends on the infrastructure and permissions of established banks rather than fintech platforms themselves.

These limitations have also shaped how competition works in the payments industry. Because banks control direct access to Fed payment rails, they remain central gatekeepers in the system. This makes it harder for newer financial companies to compete on equal terms, even when they offer faster or more user-friendly digital services.

For this reason, access to Fed payment infrastructure has become a key issue for fintech firms. Greater access is seen as a way to reduce reliance on intermediary banks, simplify payment operations, and expand the ability to build and scale financial products directly on top of core payment systems.

At the same time, the Federal Reserve’s payment systems are considered critical national financial infrastructure, which is why access has traditionally been tightly controlled to maintain stability, security, and reliability across the entire financial ecosystem.

Why the US Government Is Reviewing Fintech Access Rules

The debate over access has intensified as policymakers reassess how financial innovation should be regulated in a digital economy. The Trump administration has argued that regulatory frameworks need to evolve alongside technological change in the financial sector.

In the executive order, Trump stated that the US remains a global leader in financial innovation, driven by the rapid growth of financial technology and fintech firms. Trump wrote:

“To foster this financial innovation, the Federal Government must update regulations to allow integration of digital assets and innovative technology into traditional financial services and payment systems. The Federal Government must also remove overly burdensome and fragmented regulations and supervisory practices that form barriers to entry and primarily benefit incumbent financial services firms.”

Regulatory Concerns: The Risks of Fintech Access To the Fed Payment Infrastructure

Despite the increasing calls for accessibility, the regulators are not yet ready to permit non-bank fintechs the right of direct entry into the payment system of the Federal Reserve.

The primary concern regarding such an expansion is the potential to increase systemic risks. The Fed payment rails handle a very large amount of high-value transactions on a daily basis in the financial services industry. Increasing the base of participants who have direct access to these rails can lead to the possibility of failures or other problems, which will have a broader impact across the entire financial system.

The other major problem that needs consideration is oversight. There is already a well-structured framework available for overseeing traditional banks. Such rules are meant specifically for those organizations that make settlements by themselves. Most fintech companies, including those that are not banks, are regulated differently, and there are concerns about whether these regulations would be sufficient to grant access to more participants.

Another issue worth taking into account is that of operational resilience. Payment systems run by the Federal Reserve are expected to work faultlessly and without interruptions. There is a risk that allowing more organizations access might complicate matters and hinder efforts to maintain a proper level of security, protection against fraud, and integrity.

For this reason, access to the Federal Reserve’s payment system remains highly restricted. Any steps to open up access should entail establishing additional standards of compliance and supervision.

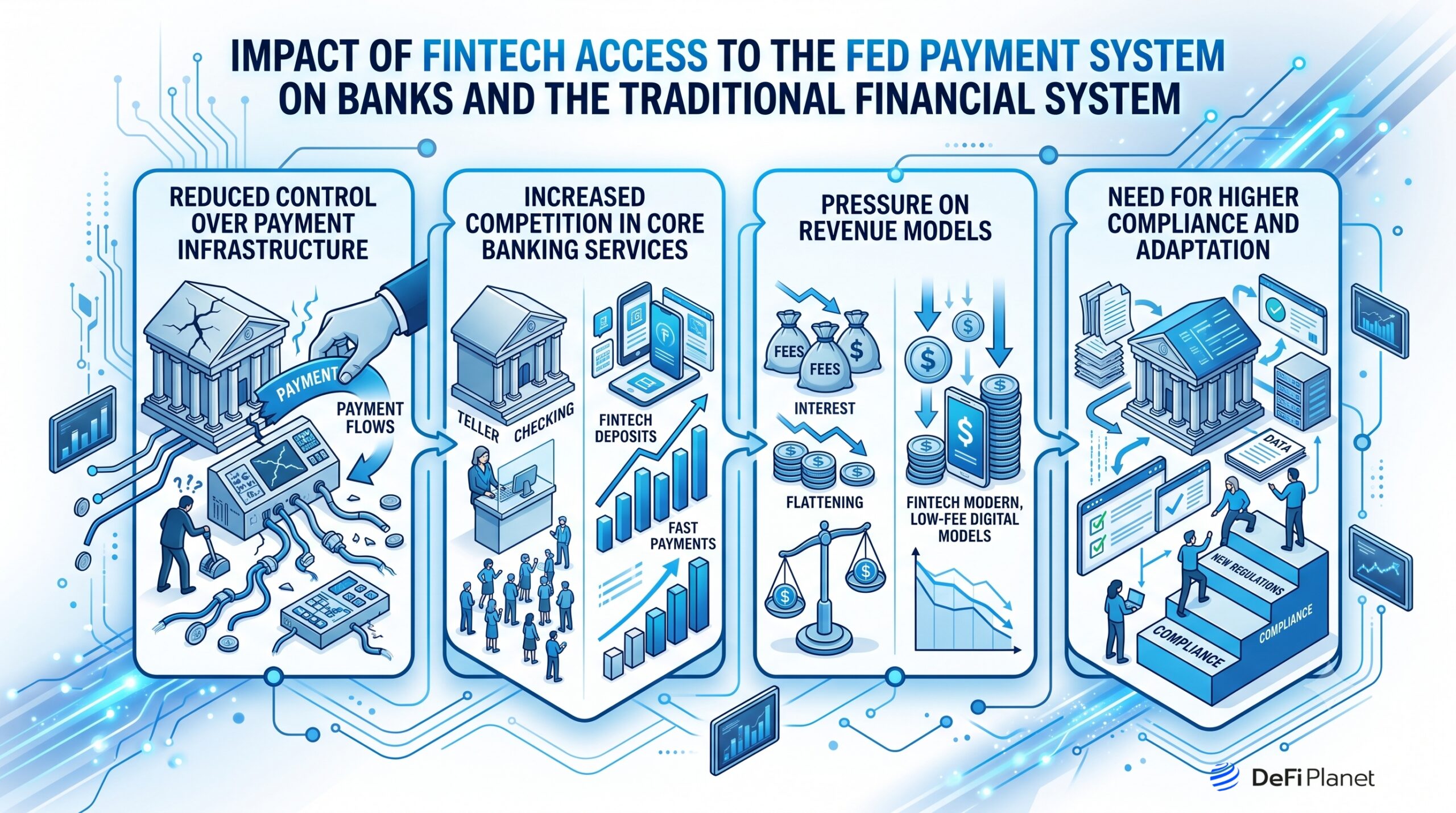

Impact On Banks and the Traditional Financial System

Expanding fintech access to the Federal Reserve’s payment systems could reshape how banks operate, compete, and maintain their role in the financial ecosystem.

Reduced control over payment infrastructure

Banks currently act as intermediaries for accessing the Federal Reserve’s payment systems. Increased access by fintechs can limit banks’ ability to maintain control over the infrastructure. It will affect their ability to control one of the most significant aspects of the financial sector.

Increased competition in core banking services

Expanded access by fintechs can increase competition in providing services traditionally offered only by banks. These include transactions and transfers. The pressure will be related to price and service delivery.

Pressure on revenue models

The banks receive a significant portion of their revenue from payment processing and transaction services. Additionally, many banks derive income from acting as intermediaries in fintech partnerships. Fintechs will find ways to avoid intermediaries, leading to losses in revenue for the bank.

Need for higher compliance and adaptation

The expansion of access will require that banks adapt to working with fintechs. This is due to the changing nature of the payment environment.

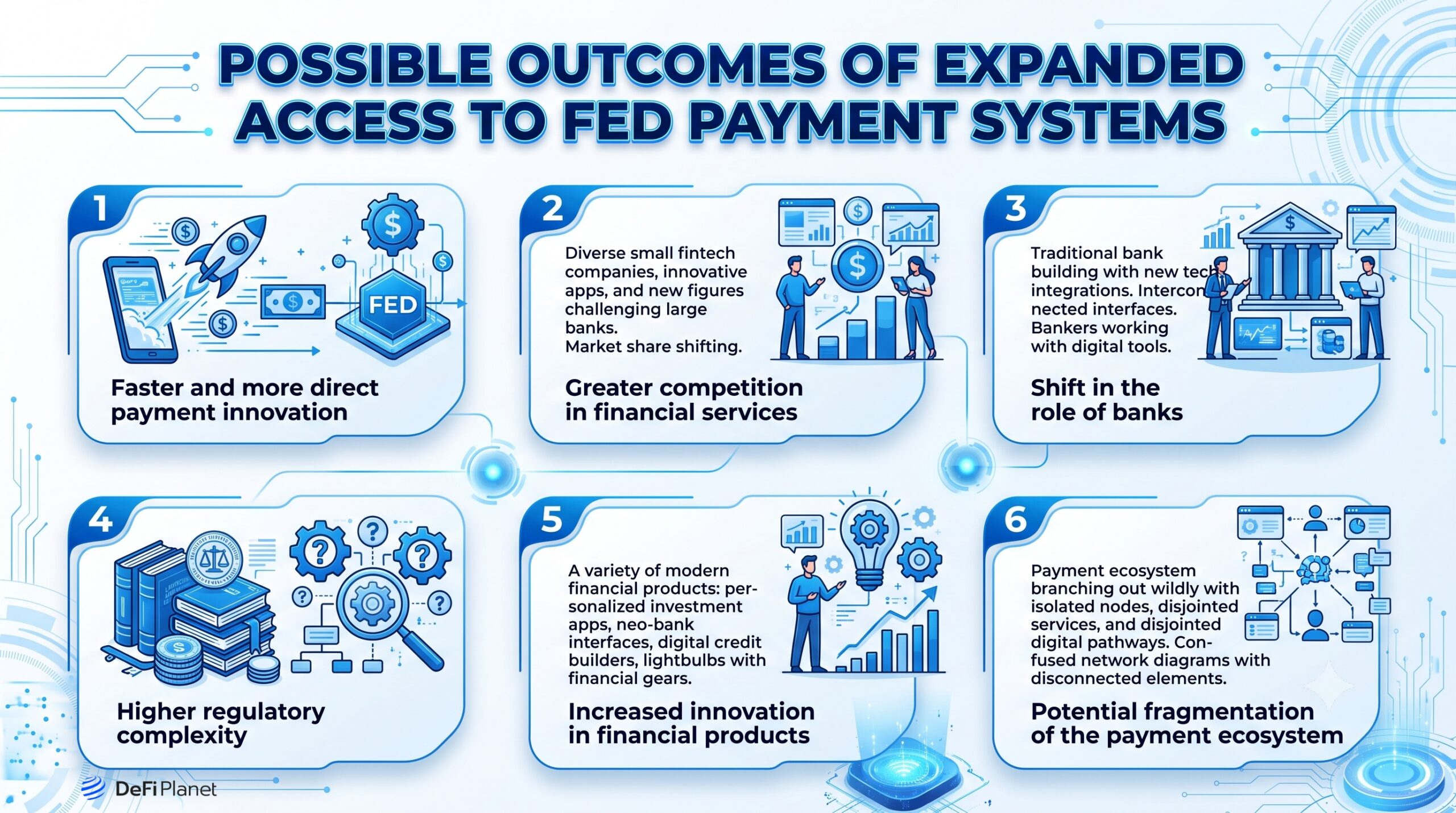

Possible Outcomes of Expanded Access to the Fed Payment System

If fintech firms gain broader access to Federal Reserve payment infrastructure, it could reshape competition, innovation, and the structure of the US financial system.

Faster and more direct payment innovation

Fintechs would be able to develop and introduce their payment solutions independently of the partnering banks. In turn, this would allow accelerating the introduction of innovations such as real-time payments, automation of various financial processes, and embedded finance. Eventually, this can accelerate the pace of implementing novel features for customers.

Greater competition in financial services

By going directly to consumers and merchants, many Fintechs would be able to compete in the payment space previously exclusive to established banks. Moreover, this is likely to lead to price competition, improved service quality, and additional consumer choices for payments and money transfers. It may also diminish the competitive edge banks hold in payment ecosystems.

Shift in the role of banks

The role of traditional banks as primary providers and gatekeepers of payment infrastructure might gradually shift towards compliance, liquidity, and risk management within Fintechs. This would mean a reduced role for banks as providers of financial services and an increased emphasis on supporting infrastructure.

Higher regulatory complexity

The increasing number of entities that directly link to the Fed infrastructure would necessitate the development of better oversight mechanisms to ensure its stability. This could involve closer scrutiny, enhanced compliance measures, and even more sophisticated tools to combat fraud and operational risk.

Increased innovation in financial products

With wider access to such a payment system, innovative financial services could be created that are currently infeasible within the framework of the bank-based financial sector. Fintech companies might find the opportunity to come up with payment services that are customized to customers’ needs.

Potential fragmentation of the payment ecosystem

With the emergence of numerous participants directly linked to the payment system, it is likely that issues stemming from the complexity and fragmentation of this environment will arise. Diverse approaches to dealing with different aspects of the payment process may complicate its operation.

Global Competitiveness Angle (EU, Chinese Fintech systems)

The debate over fintech access to the Federal Reserve’s payment systems is not only a domestic policy issue. It also has to do with how the US compares with other major economies that are already experimenting with more open or state-driven payment infrastructures.

Europe’s more open banking model

Regulations such as the Payment Services Directive 2 (PSD2) in the European Union require banks to share their customers’ account data with any third-party provider licensed to do so. This practice is known as “open banking” and makes it possible for fintechs to create innovative services built on top of conventional banking through standardized APIs.

As a result, payments, data exchange, and financial services become much more interoperable among different fintech firms. In the United States, this example puts pressure on the case for introducing a more flexible access policy to accelerate fintech development.

China’s platform-driven payments ecosystem

An entirely distinct example is China, where the fintech applications Alipay and WeChat Pay provide payment services at scale. The platforms work within an ecosystem that integrates payments, lending, and other financial services within a single ecosystem.

This example is rather effective but also demonstrates a more centralized structure with high regulatory scrutiny and the presence of only a few dominant firms.

The US is regulated but fragmented

The US occupies an intermediary position between these two systems. On the one hand, it has an extremely robust and reliable payment infrastructure. At the same time, accessibility is lower since it requires a partnership with banks.

Fintechs may have difficulty entering the core payment system through a bank, which might take more time than in more open countries overseas.

Pressure due to strategic competitiveness

As payment systems continue to develop, access to payment infrastructure may become part of strategic competitiveness in financial innovation. If US fintech businesses face more restrictions than those in Europe or Asia, the migration of innovation, investment, and skilled personnel to other regions may occur.

At the same time, loosening access in the US must be balanced against the need to maintain the security and stability of one of the world’s most critical financial networks.

Are We Headed Towards a “More Open” Infrastructure System?

The US Fed payment system looks to be moving toward gradual openness, but probably not toward a fully open system anytime soon. Pressure from fintech companies and policy-related issues may lead to greater flexibility and availability over time, especially for non-bank firms operating under certain regulations.

But the current architecture of the payment systems operated by the Fed will not undergo major changes due to the connection between the payment system and financial stability. The probable scenario is a gradual extension and increased fintech access, but only under tight regulatory control and not based on an open-architecture approach.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence.

Enjoyed this? Bookmark DeFi Planet, explore related topics, and follow us on Twitter, LinkedIn, Facebook, Instagram, Threads, and CoinMarketCap Community for seamless access to high-quality industry insights.

Take control of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics tools.

and include conclusion section that’s entertaining to read. do not include the title. Add a hyperlink to this website [http://defi-daily.com] and label it “DeFi Daily News” for more trending news articles like this

Source link

Drops 15% After Open USD Stablecoin Launch")